11.17.22

Upcoming changes to GST invoicing in New Zealand

The Inland Revenue of New Zealand is introducing a set of new rules around tax invoices, with effect from 1 April 2023. Here is a summary of the key points:

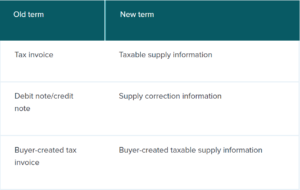

- New terminology:

Note that: businesses will not be required to change the wording on their tax invoices to reflect the new terms.

- Date for providing taxable supply information to the buyer

Sellers must provide their buyers with the taxable supply information within 28 days (or by an alternative date agreed by both parties) of a request for supplies over NZ$200.

In the case of supplies under NZ$200, sellers must keep a record of the supply, but are not required to provide taxable supply information.

- Physical record keeping is no longer required

There will be no need to maintain a single physical document containing supply information, such as a tax invoice, credit note, or debit note. All the information you need to support your GST returns may be contained in your transaction records, accounting systems, and contract documents.

- Providing Supply correct information

In the case of an incorrect amount of GST being included in the taxable supply information (currently called tax invoice), or when the seller has included an incorrect GST amount in their GST return, supply correction information (currently called credit notes or debit notes) must be provided.

Also, the Inland Revenues encourages business to adopt PEPPOL e-invoicing and has published a list of registered software providers at eInvoicing Ready product register | ATO Software Developers

Compliance is complicated

Want to learn more about how Tungsten Network makes the process of staying compliant easier?

Browse New Zealand updates

Upcoming changes to GST invoicing in New Zealand

- Country updates

The journey of e-invoicing

- Mandate information